")

Dilok Klaisataporn

LendingTree, Inc. (NASDAQ: TREE) shares fell even further after the online financial services company reported a sharper-than-expected decline in first-quarter sales and lowered its outlook for the rest of the year. After the recent price drop, TREE The stock now appears to be in a buy zone for investors with a long-term investment horizon. TREE’s stock looks attractive as the price is already reflecting the impact of negative events and there is only limited downside left. In addition to improving market dynamics, the company’s strategy of simplifying the business model and lowering the cost structure will help optimize profits in the coming years.

LendingTree Q1 earnings results and outlook

Before moving on to investment analysis, let’s briefly review LendingTree’s recent financial performance and its outlook for 2023. The earnings release highlights negative factors while emphasizing such elements could be crucial to regain investor confidence.

The negative factors

TREE’s main problem is a sales decline that started in 2022 and accelerated in the first quarter. First-quarter revenue of $200 million declined 29% year over year, marking the lowest level since the second quarter of 2020. The decline reflects tighter market conditions and slower economic expansion. Revenue fell sharply in all three businesses, including home, consumer, and insurance. Consumer sales were down 21%, insurance sales were down 4% and home sales were down 57% year over year.

The company expects revenue of $190 million in the second quarter, which means the revenue decline won’t reverse anytime soon. Additionally, the company’s projected revenue of $800 million for 2023 doesn’t appear impressive as it represents a decrease of $180 million from the midpoint of its previous 2023 guidance. The lower revenue forecast reflects not only the impact of tightening conditions, but also the impact of businesses that have already closed or will close in the coming quarters. The company’s intention to shut down its Ovation Credit Services business in the second quarter is the biggest contributor to the lower revenue guidance. The forecast also includes a drop in insurance revenue as one of its largest partners temporarily halted new policy acquisitions in several states.

The positive factors

Despite the fact that declining earnings have historically negatively impacted TREE’s stock price, the release of first-quarter results had many positives that could help investors feel more confident about future fundamentals. The two most important factors are falling costs and increasing opportunities for higher earnings growth in the coming quarters and years. For example, in the first quarter, total cost of sales fell 11.6% year over year to $13.7 million. Cost of sales is expected to continue to decrease in the coming quarters as a result of cost cutting and simplification efforts that have eliminated low-return businesses. This strategy not only reduces costs, but also allows the company to refocus on key priorities that drive profitable growth. As a result, despite lowering revenue guidance by $185 million, the company’s adjusted EBITDA guidance range was only reduced by $5 million. As the revenue environment improves, this strategy will allow the company to achieve significant operational leverage on its lower fixed cost basis.

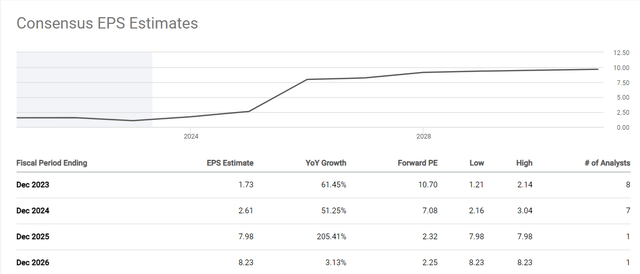

TREE Earnings Estimates (Looking for Alpha)

Analysts on Wall Street are predicting that the company’s earnings per share will be close to $1.73 in 2023, a 61% increase from this year. Earnings growth is likely to accelerate in the coming years, with 2024 likely to be another year of more than 50% growth. On the balance sheet, the company still has a significant amount of excess cash. At the end of the first quarter, the company had $150 million in cash while it only needs $50 million to $75 million to run the business.

Market trends support higher earnings expectations

Alongside cost cutting and simplification initiatives, market trends should support higher earnings forecasts. A possible pause in the Fed’s rate hike policy is the main reason behind the improving market trends. The Fed has hiked interest rates 10 times in the past 12 months, driving interest rates to levels not seen since the financial crisis. Following the latest rate hike, Fed Chair Powell said the bank was nearing or already at its target level for rate hikes.

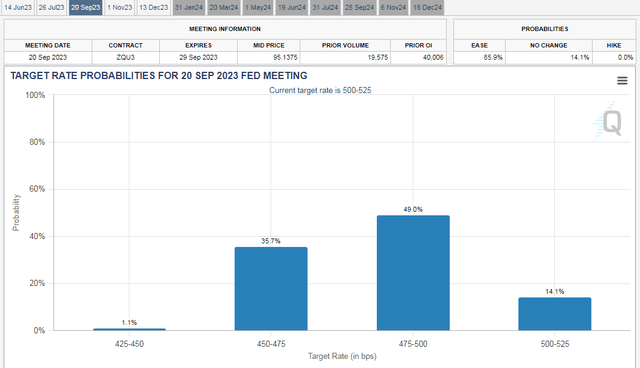

Fed rate cut expectations for September (CMEGroup)

According to CME data, the market participant also believes that the Fed’s rate hike cycle is over and a rate cut is likely in the second half of 2023. Although it appears that it will help the Fed keep interest rates at higher levels for some time to meet its goal of bringing inflation earlier, the development of banking sector tensions could force the Fed to decide in the second Interest rate cuts to be considered in the first half of the year. Several regional banks have already failed and the latest quarterly data shows banks are struggling to retain deposits and reduce loan losses. According to market analysts, bank stress would have a similar impact on the economy as the Fed’s quarter-point hike.

Why is LendingTree stock attractive now?

LendingTree Stock Price (Looking for Alpha)

Buying when others are afraid has always been the most effective strategy for generating exceptional returns. However, buying the pullback makes sense if investors are buying a stock near the bottom of the sell-off with improving fundamentals. Last year, I advised investors to stay away from TREE stock because of its deteriorating fundamentals. For more information, see my article “LendingTree: A risky gamble despite an 80% stock price drop.” But it now appears that the impact of negative events has fully reflected in the stock price. In fact, the recent sell-off of about 25% that took place after first-quarter gains shows that the impact of the lower 2023 guidance was also being felt. I believe LendingTree will gradually regain investor interest as a result of the strategies it has implemented to cut expenses and streamline its operations. That said, demand for consumer finance, housing, and insurance is likely to return once the market stabilizes, which I think will start in the second half of 2023.

TREE stock quant ratings

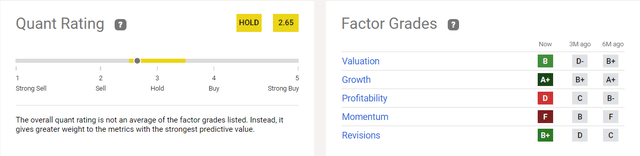

Quant Ratings (Looking for Alpha)

LendingTree received a hold rating from Seeking Alpha’s quant system with a quant score of 2.65, reflecting a low momentum and profitability score. I believe the quantitative assessment of momentum is likely to improve in the coming months as the share price has absorbed the impact of recent negative events and downside is limited. In addition, the company currently has a D rating for profitability due to losses in the previous quarters. This factor is expected to improve as the company has already returned to profitability and forecasts show solid earnings growth over the coming quarters and years. A positive B on Revisions also indicates that Wall Street analysts have started raising their earnings forecasts for the company. With a B rating, TREE’s stock appears to be a good option for dip buyers. The stock currently has a PEG ratio of 0.21 and a price-to-sales ratio of 0.25, both below the industry averages of 1.01 and 2.16, respectively. The stock also appears significantly undervalued based on its forward P/E of 10 compared to the broader market index of 17.

Finally

For investors with a long investment horizon and the potential to bear short-term volatility, LendingTree, Inc. appears to be a good choice. After a price decline of around 80% in the previous twelve months, the TREE share seems to have already priced in the effects of negative events. Additionally, buying LendingTree, Inc. makes sense as future fundamentals are expected to improve in the second half of 2023 on internal strategies and an improvement in overall market conditions.

seekingalpha.com

https://seekingalpha.com/article/4599857-lendingtree-stock-buy-the-dip-negative-events-priced-in-rating-upgrade

{kind=link}