Mark Hochleitner/iStock via Getty Images

Synopsis

Beacon Roofing Supply (NASDAQ:BECN) is a company that sells roofing and building products. BECN’s past three years’ financials have shown strong revenue growth. On top of that, its margins have been gradually expanding as well. In its preliminary FY2023 results, BECN said revenue is expected to continue growing and reach ~$9.1 billion. In terms of margins, it is expected to remain robust year-over-year. Looking ahead, demand for roofing is expected to remain strong due to its non-discretionary nature. The acquisition of Garvin and Metro Sealant is expected to strengthen its waterproofing business while Roofers Supply will support its roofing business. With the growth catalyst discussed and double-digit upside potential, I am recommending a buy rating for BECN.

Historical Financial Performance

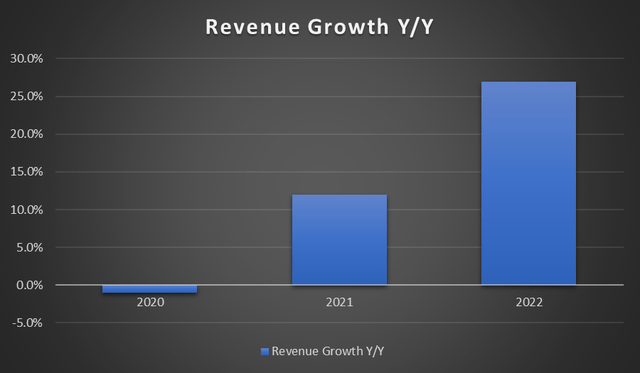

Over the past three years, BECN’s revenue has shown strong growth. In 2021, it reported growth of 12.3%, driven by strong demand for residential and complementary products. In 2022, it continued to report strong revenue growth of 26.9%, driven by strong pricing, volume, and acquisitions.

Seeking Alpha

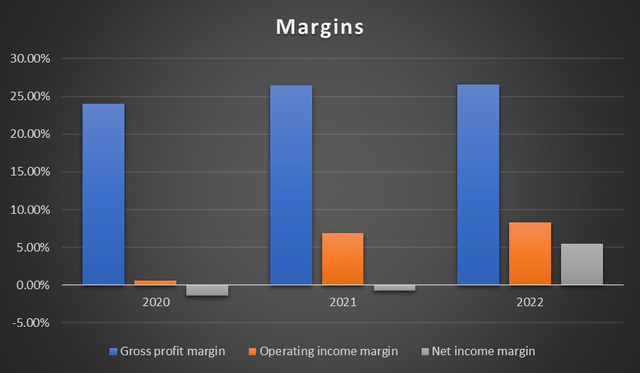

In terms of profitability, it’s clear that BECN’s margins have been expanding over the years as well. In 2021, gross profit margins expanded to 26.5% from 24%, and this was driven by price increase. In 2022, gross profit margins stayed consistent with 2021’s level.

In 2021, its operating income margin expanded significantly from 0.6% to 6.9%. The expansion was driven by a higher gross profit margin, a reduction in SG&A as a percentage of revenue, and a $158.6 million decrease in amortization expense. In 2022, operating income margin expanded from 6.9% to 8.3%, which was driven by a further reduction in SG&A as a percentage of revenue from 17.1% to 16.3%. As a result, BECN’s net income benefited. In 2022, it reported a positive net income margin of 5.44%, up from the previous period’s negative 0.7%.

Seeking Alpha

3Q23 Earnings Analysis

BECN reported a strong 3Q23 earnings result as net sales grew 7% year-over-year to $2.58 billion, up from 3Q22’s $2.41 billion. This strong growth is mainly attributed to its successful acquisitions and greenfield initiatives. For its residential roofing products segment, which accounts for 53.1% of the sales mix, sales were up 13.6% year-over-year, and this growth was mainly driven by higher volume. Its complementary product, which accounts for 20.8% of the sales mix, grew 12.7% year-over-year, and this growth is mainly due to the acquisition of Coastal Construction Products. However, its non-residential roofing product, which accounts for 26.1% of the sales mix, was down 7.6% year-over-year.

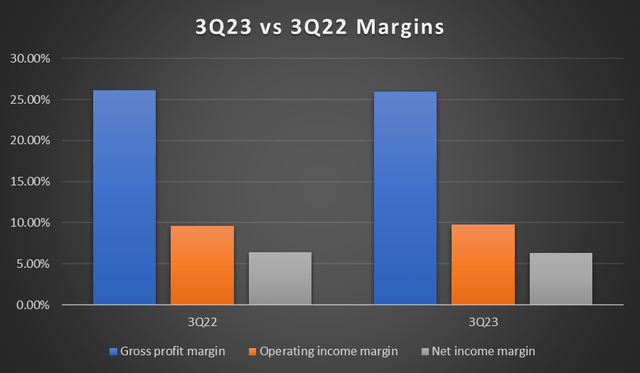

Moving onto profitability margins, they have remained robust year-over-year. All three margins are in line with 3Q22’s level. In 3Q23, gross profit margin reported was 26% vs. 3Q22’s 26.1%, operating income margin was 9.8% vs. 9.6%, and net income margin was 6.3% vs. 6.4%. Next, I would like to address its reported diluted EPS. For 3Q23, diluted EPS was negative $4.16 vs. 3Q22’s positive $1.95. The negative EPS is due to the $414.6 million preferred shares repurchase premium.

Seeking Alpha

4Q23 Preliminary Results

Based on BECN’s announcement, its 4Q23 results are set to be released on 27 February 2024. However, on 10 January 2024, it released its preliminary 4Q23’s results. For 4Q23, net sales are anticipated to be ~$2.3 billion, up from 4Q22’s ~$1.9 billion.

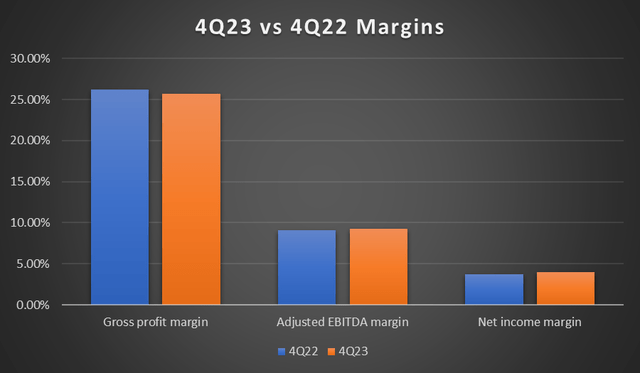

In terms of profitability, 4Q23’s gross profit margin is anticipated to be ~25.7% vs. 4Q22’s 26.2%, which is down slightly. Its net income is expected to be between $92 and $96 million, which has a midpoint of $94 million vs. 4Q22’s $73.3 million. Using the midpoint, 4Q23’s net income margin is ~4.1% vs. 4Q22’s 3.7%.

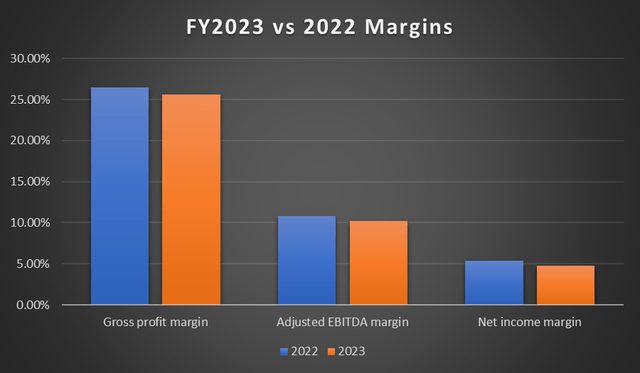

Lastly, 4Q23’s diluted net income per share is estimated to be between $1.42 and $1.48, with a midpoint of $1.45 per share. Looking at the following chart, it’s clear that 4Q23’s preliminary results’ margins [gross profit margin, adjusted EBITDA margin, net income margin] have remained robust as they are in line with 4Q22.

Seeking Alpha

For FY2023, net sales are anticipated to reach ~$9.1 billion vs. FY2022’s $8.43 billion, representing growth of ~7.9%. Gross margin is estimated to be ~25.6% vs. FY2022’s 26.5%, down by ~0.9%, which is modest in my opinion. In terms of net income, FY2023 is expected to be between $432 million and $436 million, with a midpoint of $434 million compared to FY2022’s $458 million. FY2023’s net income margin is ~4.8% vs. FY2022’s 5.4%, which is down ~0.6%. Lastly, adjusted EBITDA is expected to reach between $925 and $930 million, which represents a margin of ~10.2% at the midpoint vs. FY2022’s $910 million with a margin of 10.8%.

Seeking Alpha

Strong Asphalt Shingle Demand

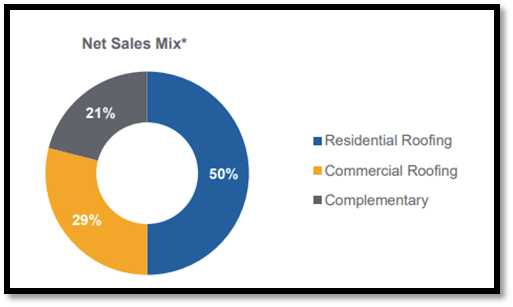

Based on the following, residential roofing accounts for 50% of the sales mix, with commercial roofing coming in second at 29%. The remaining 21% is made up of complementary. In total, roofing accounts for most of its sales.

BECN’s Investor Relations

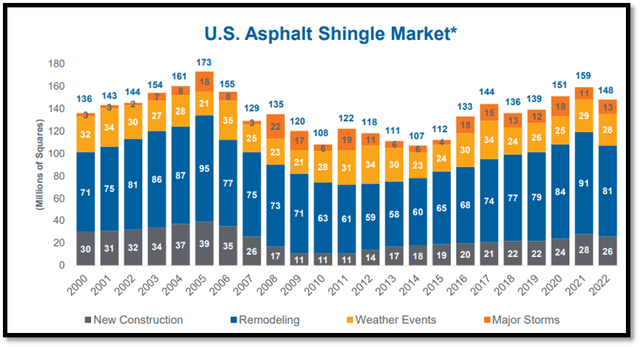

In 2005, the US asphalt shingle market reached 173 million of squares. As of 2022, it has only reached 148 million of squares, which remains well below 2005’s level. Based on the chart, it is clear that the demand for roofing is mainly driven by remodeling, weather events, and major storms. In 2022, these three segments accounted for ~82% of total demand. Since 2010, the roofing market has been consistently growing, from 108 million in 2010 to 148 million in 2022, showing a robust demand trend.

BECN’s Investor Relations

Re-roofing Main Drivers are Non-Discretionary

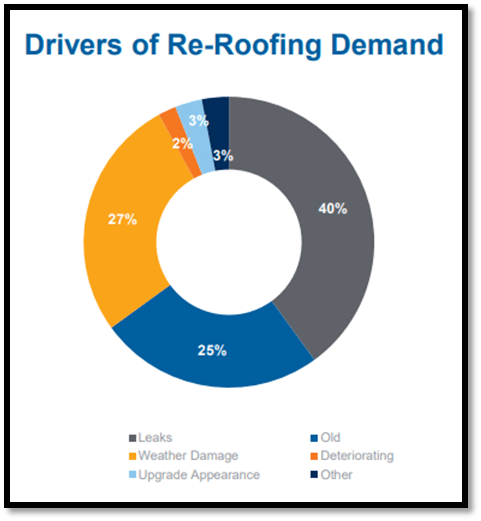

Leakage accounts for 40% of re-roofing demand, 25% is due to age, and 27% is due to weather damage. In total, they account for 92% of total demand. Leaks, age, and weather damage are considered to be non-discretionary in nature as they are essential repairs. When an expense is non-discretionary in nature, spending on such expense is generally not impacted by macro-uncertainties such as a recession or slower economic growth. Therefore, BECN’s demand outlook for re-roofing is expected to be robust for the foreseeable future.

BECN’s Investor Relations

Acquisitions in 2023 and 2024 that Drive Growth

In order to fuel future growth, BECN has been actively acquiring companies. During the quarter, it executed on the acquisition pipeline with five new acquisitions. One of the more prominent acquisitions is in regards to Garvin Construction Products. This acquisition is anticipated to significantly strengthen BECN’s waterproofing category. This segment is largely considered to be non-discretionary, just like its roofing business. Lastly, the acquisition of Garvin Construction Products adds five more locations for BECN, further improving its presence in the Northeast.

In addition to Garvin, BECN has also announced its acquisition of Roofers Supply of Greenville on 1 February 2024. The aim of this acquisition is to expand BECN’s reach, expand its offerings within Carolina, and help BECN achieve their goal of being the number one commercial roofing company in the US. The acquisition of Roofers Supply of Greenville is the first acquisition to be announced for 2024.

The second acquisition announced in 2024 is in regards to Metro Sealant and Waterproofing Supply. For more than 30 years, Metro Sealant has specialized in providing customized sealant and waterproofing solutions to contractors, design experts, and property owners in the commercial construction sector. The purpose of acquiring Metro Sealant & Waterproofing Supply is to support and strengthen its waterproofing division, the same as the acquisition of Garvin Construction Products.

With these well-targeted acquisitions, BECN has positioned itself well for future growth as they expand its roofing and waterproofing businesses. These acquisitions align with their strategic goals and are poised to bolster BECN’s growth outlook.

Relative Valuation Model

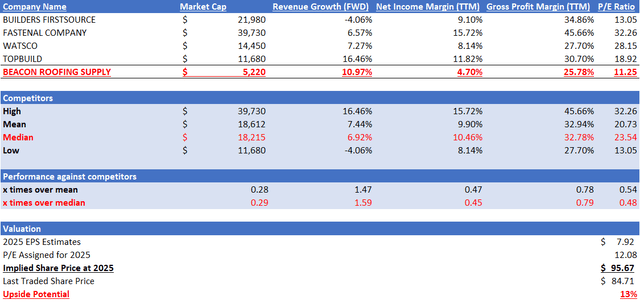

In terms of company size, BECN is significantly smaller than its competitors. BECN’s market capitalization is $5.22 billion vs. its competitors’ median of $18.2 billion. BECN is only ~29% the size of its competitors. Despite its smaller size, it outperformed its competitors in terms of growth outlook. BECN’s forward revenue growth rate is 10.97% vs. its competitors’ median of 6.92%.

However, when it comes to profitability margins, BECN underperformed its competitors. In terms of gross profit margin TTM, BECN reported 25.78%, while its competitors’ median is 32.78%, which represents 0.79x over the median. In terms of net income margin TTM, BECN also reported lower figures. Its reported 4.7% vs. its competitors’ median of 10.46%.

Currently, BECN’s forward P/E ratio is trading at 11.25x, lower than its competitors’ median of 23.54x. In addition, it is also below its own 5-year average of 12.08x. Given the growth catalyst I have discussed above and its better forward revenue growth rate, I argue that BECN’s P/E ratio should be at least trading in line with its historical average of 12.08x.

In 2022, it reported EPS of $7.86. For 2023, the market estimates that its EPS is anticipated to be $7.42, while for 2024, it will be $7.92. Given its consistent EPS growth over the years and the growth catalyst discussed above, the market estimate is justified. By applying its 5-year average P/E to its 2024 EPS estimate, my implied share price is $95.67. Compared to its last traded share price, the upside potential is ~13%.

Author’s Valuation Model

Risk

The downside risk of buying BECN is in relation to the potential impact of macroeconomic factors on the demand for residential housing and commercial construction activity. During the quarter, macro factors negatively impacted new builds and existing for-sale units. In addition, commercial construction activity was slower than expected.

As mentioned by management in their annual report, re-roofing activities account for ~80% of total roofing demand. This means that the remaining 20% belongs to new construction. Although new construction accounts for a smaller portion of total demand, 20% is still quite significant. Therefore, if the macroeconomic environment turns south and negatively impacts housing and commercial construction activity, BECN’s demand outlook might be affected.

Conclusion

In conclusion, BECN’s past financial results have demonstrated strong revenue growth. In addition, margins over the years have been expanding consistently as well. In its preliminary FY2023 results, revenue is expected to grow to ~$9.1 billion, while its margins are expected to remain robust year-over-year. Looking ahead, roofing demand is expected to remain strong, as the demand is mainly driven by remodeling, leakage, age, and weather damage. These are considered non-discretionary in nature as they are essential repairs. Therefore, demand will not as much fluctuate with macroeconomic factors. In addition, the acquisition of Garvin Construction Products and Metro Sealant is expected to strengthen its waterproofing business, and this business are considered non-discretionary as well. Therefore, I anticipate that BECN’s strategic acquisitions will contribute positively to its growth outlook. With double-digit upside potential, I am recommending a buy rating.

seekingalpha.com

https://seekingalpha.com/article/4670025-beacon-roofing-supply-drivers-of-roofing-demand-are-non-discretionary

{kind=link}